| Heading | : | AMENDMENT IN INCOME TAX RULE 30, 31, 31A AND FORM 26Q, 26QB, 26QC AND 26QD AND INSERTION OF NEW FORM 16E AND 26QE. |

|---|

AMENDMENT IN INCOME TAX RULE 30, 31, 31A AND FORM 26Q, 26QB, 26QC AND 26QD AND INSERTION OF NEW FORM 16E AND 26QE.

MINISTRY OF FINANCE

(Department of Revenue)

(CENTRAL BOARD OF DIRECT TAXES)

New Delhi

G.S.R. 463(E).– In exercise of the powers conferred by section 295 read with sections 194B, 194-IA, 194R, 194S and section 206AB of the Income-tax Act, 1961, the Central Board of Direct Taxes, hereby, makes the following rules further to amend the Income-tax Rules, 1962, namely:-

1. Short title and commencement.– (1) These rules may be called the Income-tax (19th Amendment) Rules, 2022.

(2) Save as otherwise provided in these rules, they shall come into force from the date of their publication in the Official Gazette.

2. In the Income-tax Rules, 1962 (hereinafter referred to as the principal rules), (a) in rule 30, with effect from the 1st July, 2022––

(i) after sub-rule (2C), the following sub-rule shall be inserted, namely:––

“(2D) Notwithstanding anything contained in sub-rule (1) or sub-rule (2), any sum deducted under section 194S by a specified person referred to in that section shall be paid to the credit of the Central Government within a period of thirty days from the end of the month in which the deduction is made and shall be accompanied by a challan-cum-statement in Form No. 26QE.”;

(ii) after sub-rule (6C), the following sub-rule shall be inserted, namely:––

“(6D) Where tax deducted is to be deposited accompanied by a challan-cum-statement in Form No.26QE, the amount of tax so deducted shall be deposited to the credit of the Central Government by remitting it electronically within the time specified in sub-rule (2D) into the Reserve Bank of India or the State Bank of India or any authorised bank.”;

(b) in rule 31, after sub-rule (3C), the following sub-rule shall be inserted with effect from the 1st July, 2022, namely:–

“(3D) Notwithstanding anything contained in sub-rule (1) or sub-rule (2) or sub-rule (3), every person, being a specified person referred to in section 194S and responsible for deduction of tax under that section shall furnish the certificate of deduction of tax at source in Form No.16E to the payee within fifteen days from the due date for furnishing the challan-cum-statement in Form No.26QE under rule 31A after generating and downloading the same from the web portal specified by the Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems) or the person authorised by him.”;

(c) in rule 31A, with effect from the 1st day of July, 2022––

(i) in sub-rule (4), after clause (xvi), the following clause shall be inserted, namely:–– “(xvii) furnish particulars of amount deposited being prerequisite for releasing––

(a) winnings in terms of proviso to section 194B;

(b) benefit or perquisite in terms of first proviso to sub-section (1) of section 194R; and

(c) consideration in terms of proviso to sub-section (1) of section 194S along with the challan details such as BSR code of the bank, date of payment and challan serial number.”

(ii) after sub-rule (4C), the following sub-rule shall be inserted, namely,––

“(4D) Notwithstanding anything contained in sub-rule (1) or sub-rule (2) or sub-rule (3) of sub-rule (4), every specified person referred to in section 194S and responsible for deduction of tax under that section shall furnish to the Principal Director General of Income-tax (Systems) or Director General of Income-tax (Systems) or the person authorised by the Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems), a challan-cum-statement in Form No. 26QE electronically in accordance with the procedures, formats and standards specified under sub-rule (5) within thirty days from the end of the month in which the deduction is made.”.

3. In the principal rules, in Appendix II, after Form No. 16D, the following Form shall be inserted with effect from the 1st July, 2022, namely,––

|

“Form No. 16E |

|||||||||

|

[See rule 31(3D)] |

|||||||||

|

Certificate under section 203 of the Income-tax Act, 1961 for tax deducted at source |

|||||||||

|

Certificate No. |

Last updated on |

||||||||

|

Name and address of the Deductor |

Name and address of the Deductee |

||||||||

|

Permanent Account Number or Aadhaar |

Permanent Account Number or Aadhaar |

Financial Year of deduction |

|||||||

|

Summary of Transaction(s) |

|||||||||

|

S. No. |

Unique Acknowledgement |

Amount paid/credited |

Date of payment/credited |

Amount of tax deducted and |

|||||

|

Total (Rs.) |

|||||||||

|

DETAILS OF TAX DEPOSITED TO THE CREDIT OF THE CENTRAL GOVERNMENT FOR WHICH CREDIT IS TO BE GIVEN TO THE DEDUCTEE |

|||||||||

|

S. No. |

Amount of tax deposited in |

Challan Identification number (CIN) |

|||||||

|

BSR Code of the Bank Branch |

Date on which tax deposited |

Challan Serial |

|||||||

|

1. |

|||||||||

|

2. |

|||||||||

|

Total (Rs.) |

|||||||||

|

Verification |

|||||||||

|

I, ……………. ., son/daughter of……………. in the capacity of…….. (designation) do hereby certify that a sum of (Rs.) ………………. [Rs. ………… . (in words)] has been deducted and deposited to the credit of the Central Government. I further certify that the information given above is true, complete and correct and is based on the books of account, documents, challan-cum-statement of deduction of tax, TDS deposited and other available records. |

|||||||||

|

Place |

(Signature of person responsible for deduction of tax) |

||||||||

|

Date |

Full name: ”. |

||||||||

4. In the principal rules, in Appendix II, in form 26Q, with effect from the 1st day of July, 2022 ––

(a) for the brackets, words, figures and letters “[See sections 192A, 193, 194, 194A, 194B, 194BB, 194C, 194D, 194DA, 194EE, 194F, 194G, 194H, 194-I, 194J, 194K, 194LA, 194LBA, 194LBB, 194LBC, 194N, 194-O, 194P, 194Q, 197A, 206AA, 206AB and rule 31A] ”, the following brackets, words, figures and letters, shall be substituted, namely:––

“[See sections 192A, 193, 194, 194A, 194B, 194BB, 194C, 194D, 194DA, 194EE, 194F, 194G, 194H, 194-I, 194J, 194K, 194LA, 194LBA, 194LBB, 194LBC, 194N, 194-O, 194P, 194Q, 194R, 194S, 197A, 206AA, 206AB and rule 31A] ”;

(b) for the “Annexure”, the following “Annexure” shall be substituted, namely:––

“ANNEXURE: DEDUCTEE/PAYEE WISE BREAK UP OF TDS

(Please use separate Annexure for each line-item in Table at Sl. No. 4 of main Form 26Q)

|

BSR Code of branch/Receipt Number of Form No. 24G |

|

|

Date on which challan deposited/Transfer voucher date (dd/mm/yyyy) |

|

|

Challan Serial Number / DDO Serial No. of Form No. 24G |

|

|

Amount as per Challan |

|

|

Total tax to be allocated among deductees/ payees as in the vertical total of Col. 421 |

|

|

Total interest to be allocated among the deductees/payees mentioned below |

–

|

Name of the Deductor/Payer |

|

|

TAN |

–

Sl. No. |

Dedu-ctee

|

Dedu-ctee/ payee

|

PAN of

|

Name of the deduct ee/ payee |

Section code (See Note 17) |

Date of payment or credit (dd/m m/ yyyy) |

Amount

|

Amount of cash withd-rawal in excess of Rs. 1 crore as referred to in section 194N (in cases not covered by the first proviso to section 194N) |

Amount of cash

|

Amount of cash withd-rawal in excess of Rs. 1 crore for cases covered by sub-clause(b) of clause (ii) of first prov-ison to section 194N |

Total

|

Total tax depo-sited |

Date of

|

Rate at

|

[412] |

[413] |

[414] |

[415] |

[416] |

[417] |

[418] |

[419] |

[419A] |

[419B] |

[419C] |

[420] |

[421] |

[422] |

[423] |

1 |

||||||||||||||

2 |

||||||||||||||

3 |

||||||||||||||

Total |

–

Reason for

|

Number

|

If section code 94B-P is selected, then provide |

If section code 94R-P is selected, then provide |

If section code 94S-P is selected, then provide |

|||||||||

Amount

|

BSR

|

Date of payment |

Challan

|

Amount

|

BSR

|

Date of payment |

Challan

|

Amount

|

BSR

|

Date of payment |

Challan

|

||

[424] |

[425] |

[426A] |

[426B] |

[426C] |

[426D] |

[427A] |

[427B] |

[427C] |

[427D] |

[428A] |

[428B] |

[428C] |

[428D] |

Verification

I,…………………………………………………………………………. , hereby certify that all the particulars furnished above are correct and complete.

Place: …………………..

Date: …………………..

…………………………………………..

Signature of the person responsible for deducting tax at source

……………………………………………

Name and designation of the person responsible for deducting tax at source

Notes:

1. Write “A” if “lower deduction” or “no deduction” is on account of a certificate under section 197.

2. Write “B” if no deduction is on account of declaration under section 197A other than the cases mentioned in sub-section (1F) of section 197A.

3. Write “C” if deduction is on higher rate under section 206AA on account of non-furnishing of PAN.

4. Write “D” if no deduction or lower deduction is on account of payment made to a person or class of person on account of notification issued under sub-section (5) of section 194A.

5. Write “E” if no deduction is on account of payment being made to a person referred to in Board Circular No. 3 of 2002 dated 28th June 2002 or Board Circular No. 11 of 2002 dated 22nd November 2002 or Board Circular No. 18/2017 dated 29th May 2017.

6. Write “Y” if no deduction is on account of payment below threshold limit specified in the Income-tax Act, 1961.

7. Write “T” if no deduction is on account of deductee or payee being transporter. PAN of deductee or payee is mandatory [section 194C(6)].

8. Write “Z” if no deduction or lower deduction is on account of payment being notified under section 197A(1F).

9. Write “M” if no deduction or lower deduction is on account of notification issued under second proviso to section 194N.

10. Write “N” if no deduction or lower deduction is on account of payment made to a person referred to in the third proviso to section 194N or on account of notification issued under fourth proviso to section 194N.

11. Write “O” if no deduction is as per the provisions of sub-section (2A) of section 194LBA.

12. Write “P” if no deduction is on account of payment of dividend made to a business trust referred to in clause (d) of second proviso to section 194 or in view of any notification issued under clause (e) of the second proviso to section 194.

13. Write “Q” if no deduction in view of payment made to an entity referred to in clause (x) of sub -section (3) of section 194A.

14. Write “S” if no deduction is in view of the provisions of sub-section (5) of section 194Q.

15. Write “T” if the deduction is on higher rate in view of section 206AB for non-filing of return of income.

16. List of section codes is as under:

|

Section |

Nature of Payment |

Section Code |

|

192A |

Payment of accumulated balance due to an employee |

192A |

|

193 |

Interest on securities |

193 |

|

194 |

dividend |

194 |

|

194A |

Interest other than interest on securities |

94A |

|

194B |

Winnings from lotteries and crossword puzzles |

94B |

|

Proviso to section 194B |

Winnings from lotteries and crossword puzzles where consideration is made in kind or cash is not sufficient to meet the tax liability and tax has been paid before such winnings are released |

94B-P |

|

194BB |

Winnings from horse race |

4BB |

|

194C |

Payment of contractors and sub-contractors |

94C |

|

194D |

Insurance Commission |

94D |

|

194DA |

Payment in respect of life insurance policy |

4DA |

|

194EE |

Payments in respect of deposits under National Savings Schemes |

4EE |

|

194F |

Payments on account of repurchase of Units by Mutual Funds or UTIs |

94F |

|

194G |

Commission, prize etc., on sale of lottery tickets |

94G |

|

194H |

Commission or Brokerage |

94H |

|

194-I(a) |

Rent |

4-IA |

|

194-I (b) |

Rent |

4-IB |

|

194J(a) |

Fees for Technical Services (not being professional service), royalty for sale, distribution or exhibition of cinematographic films and call center (@2%) |

94J-A |

|

194J(b) |

Fee for professional service or royalty etc. (@10%) |

94J-B |

|

194K |

Income in respect of units |

94K |

|

194LA |

Payment of Compensation on acquisition of certain immovable property |

4LA |

|

194LBA(a) |

Certain income in the form of interest from units of a business trust to a resident unit holder |

4BA1 |

|

194LBA(b) |

Certain income in the form of dividend from units of a business trust to a resident unit holder |

4BA2 |

|

194LB |

Income in respect of units of investment fund |

LBB |

|

194LBC |

Income in respect of investment in securitization trust |

LBC |

|

194N |

Payment of certain amounts in cash |

94N |

|

First proviso to section194N |

Payment of certain amounts in cash to non-filers |

94N-F |

|

194-O |

Payment of certain sums by e-commerce operator to e-commerce participant |

94O |

|

194P |

Deduction of tax in case of specified senior citizens |

94P |

|

194Q |

Payment of certain sums for purchase of goods |

94Q |

|

194R |

Benefits or perquisites of business or profession* |

94R |

|

First Proviso to |

Benefits or perquisites of business or profession where such benefit is provided in kind or where part in cash is not sufficient to meet tax liability and tax required to be deducted is paid before such benefit is released* |

94R-P |

|

194S |

Payment of consideration for transfer of virtual digital asset by persons other than specified persons* |

94S |

|

Proviso to sub- |

Payment for transfer of virtual digital asset where payment is in kind or in exchange of another virtual digital asset and tax required to be deducted is paid before such payment is released* |

94S-P |

* Note:–– In relation to section 194R and section 194S, the changes shall come into effect from 1st July, 2022.”.

5. In the principal rules, in Appendix II, for Form 26QB, the following Form shall be substituted, namely,––

“Form No. 26QB

[See section 194-IA, rule 30 and rule 31A]

Challan-cum-statement of deduction of tax under section 194-IA

|

Financial Year |

– |

Major Head Code* |

Minor Head |

|||||||||||||||||||||||

|

Permanent Account Number or Aadhaar Number of Transferee /Payer/Buyer |

||||||||||||||||||||||||||

|

Category of Permanent Account Number* |

Status of PAN* |

|||||||||||||||||||||||||

|

Full Name of Transferee/Payer/Buyer |

||||||||||||||||||||||||||

|

Complete Address of Transferee/Payer/Buyer |

||||||||||||||||||||||||||

|

PIN |

||||||||||||||||||||||||||

|

Mobile No. |

ID |

|||||||||||||||||||||||||

|

Whether more than one transferee/payer/buyer (Yes/No) |

||||||||||||||||||||||||||

|

Permanent Account Number or Aadhaar Number of Transferor /Payee/Seller |

||||||||||||||||||||||||||

|

Category of Permanent Account Number* |

Status of |

|||||||||||||||||||||||||

|

Full Name of Transferor/Payee/Seller |

||||||||||||||||||||||||||

|

Complete Address of Transferor/Payee/Seller |

||||||||||||||||||||||||||

|

PIN |

||||||||||||||||||||||||||

|

Mobile No. |

ID |

|||||||||||||||||||||||||

|

Whether more than one Transferor/Payee/Seller (Yes/No) |

||||||||||||||||||||||||||

|

Complete Address of Property transferred |

||||||||||||||||||||||||||

|

PIN |

||||||||||||||||||||||||||

|

Date of agreement/ booking** |

Total Value of Consideration (amount in Rs.) |

Payment in installment or lumpsum |

||||||||||||||||||||||||

|

Whether TDS is deducted at Higher rate as per section 206AB (Yes/No)*** |

||||||||||||||||||||||||||

|

Whether it is last instalment? |

Yes………… No…… |

|||||||||||||||||||||||||

|

Total amount paid/ credited in previous installments, if any (in Rs.) (A) |

Amount paid/ credited currently (B) |

Total Stamp duty value of the Property (in Rs.) (C) |

Amount on which TDS to be deducted (D) (see note 1) |

Date of payment/ credit** |

Rate at which deducted (see note 2) |

Amount of tax deducted at source (see note 3) |

Date of Deduction** |

|||||||||||||||||||

|

Whether stamp duty value is higher than sale consideration |

||||||||||||||||||||||||||

|

Date of Deposit** |

Mode of payment |

Simultaneously e-tax payment |

e-tax payment on subsequent date |

|||||||||||||||||||||||

|

Details of payment of tax deducted at source (amount in Rs.) |

||||||||||||||||||||||||||

|

TDS (Income Tax)(Credit of tax to the deductee shall be given for this amount |

||||||||||||||||||||||||||

|

Interest |

||||||||||||||||||||||||||

|

Fee |

||||||||||||||||||||||||||

|

Total Payment |

||||||||||||||||||||||||||

|

Total payment in words (in Rs.) |

||||||||||||||||||||||||||

|

Crores |

Lakhs |

Thousands |

Hundreds |

Tens |

Units |

|||||||||||||||||||||

|

Unique Acknowledgement no. (generated by TIN) |

||||||||||||||||||||||||||

*To be updated automatically

**In dd/mm/yyyy format

*** From 1st April, 2022, provisions of section 206AB are not applicable in case of tax deduction under section 194-IA.

Notes:

1. (a) In case of installment, where it is not last installment, (A+B);

(b) in any other case (i.e., last installment or lump sum payment), (A+B) or (C), whichever is higher.

2. Tax to be deducted at higher rates in case provisions of section 206AB is applicable. ***

3. (a) In case of installment, where it is not last installment, TDS on (A+B) as reduced by the TDS in earlier instalments, if any;

(b) In any other case (i.e., last installment or lump sum payment), TDS on (A+B) or (C), whichever is higher, as reduced by TDS paid on earlier instalments, if any.”.

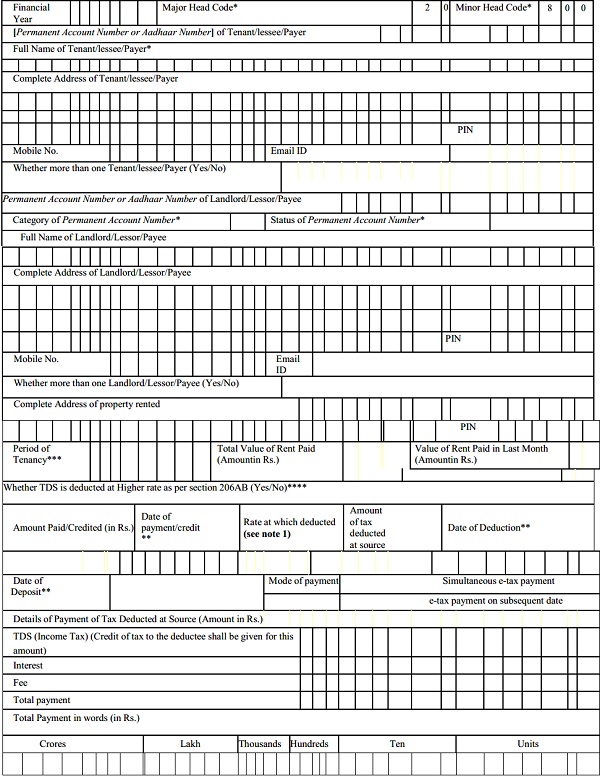

6. In the principal rules, in Appendix II, for Form 26QC, the following Form shall be substituted, namely:––

“FORM NO. 26QC

[See section 194-IB, rule 30(2B) and (6B) and rule 31A(4B)]

Challan-cum-statement of deduction of tax under section 194-IB

*To be updated automatically

**In dd/mm/yyyy format.

***Against period of tenancy, the number of months the property is rented for the financial year may be mentioned.

****From 1st April, 2022, provisions of section 206AB are not applicable in case of deduction under section 194-IB.

Note: Tax to be deducted at higher rates in case provisions of section 206AB is applicable. ****”.

7. In the principal rules, in Appendix II, for Form 26QD, the following Form shall be substituted, namely,––

Form No.26QD

[See section 194M, rule 30(2C), rule 30(6C) and rule 31A (4C)]

Challan-cum-statement of deduction of tax under section 194M

* To be updated automatically

** In dd/mm/yyyy format.

*** From 1st April, 2022, provisions of section 206AB are not applicable in case of deduction under section 194M.

Note: Tax to be deducted at higher rates in case provisions of section 206AB is applicable. ***”.

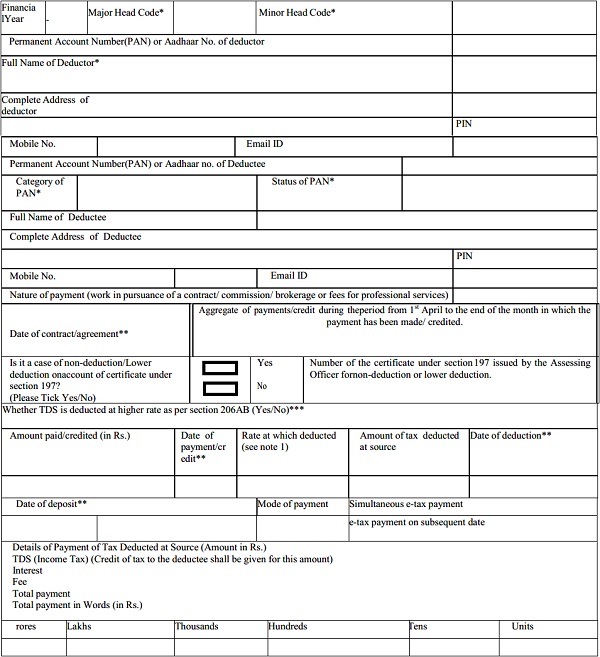

8. In the principal rules, in Appendix II, after Form 26QD, the following Form shall be inserted with effect from 1st July, 2022, namely:––

“Form No. 26QE

[See section 194S, rule 30 (2D) and (6D) and rule 31A(4) and (4D)]

Challan-cum-statement of deduction of tax under section 194S by specified persons

“Form No. 26QE

[See section 194S, rule 30 (2D) and (6D) and rule 31A(4) and (4D)]

Challan-cum-statement of deduction of tax under section 194S by specified persons

|

Financial Year |

– |

Major Head |

Minor Head Code* |

|||||||||||||||||||||||||||||||||||||

|

Permanent Account Number or Aadhaar Number of deductee |

||||||||||||||||||||||||||||||||||||||||

|

Category of Permanent Account Number* |

Status of PAN* |

|||||||||||||||||||||||||||||||||||||||

|

Full Name of deductee |

||||||||||||||||||||||||||||||||||||||||

|

Complete Address of deductee |

||||||||||||||||||||||||||||||||||||||||

|

PIN |

||||||||||||||||||||||||||||||||||||||||

|

Mobile No. |

Email ID |

|||||||||||||||||||||||||||||||||||||||

|

Permanent Account Number or Aadhaar Number of deductor |

||||||||||||||||||||||||||||||||||||||||

|

Category of Permanent Account Number* |

Status of PAN* |

|||||||||||||||||||||||||||||||||||||||

|

Full Name of deductor |

||||||||||||||||||||||||||||||||||||||||

|

Complete Address of deductor |

||||||||||||||||||||||||||||||||||||||||

|

PIN |

||||||||||||||||||||||||||||||||||||||||

|

Mobile No. |

Email ID |

|||||||||||||||||||||||||||||||||||||||

|

Date of transfer of |

Total Value of Consideration (amount in Rs.) |

Whether payment made in kind or in exchange of another VDA |

YES |

|||||||||||||||||||||||||||||||||||||

|

If yes, then provide |

Challan |

BSR code of bank branch |

Date on which tax deposited |

Challan serial number |

||||||||||||||||||||||||||||||||||||

|

Amount of tax paid (in Rs.) |

||||||||||||||||||||||||||||||||||||||||

|

Amount paid/ credited either in cash or kind or in exchange of another VDA (in Rs.) |

Date of payment/ |

Rate at which deducted |

Amount of tax deducted at source |

Date of Deduction** |

||||||||||||||||||||||||||||||||||||

|

Date of Deposit** |

Mode of payment |

Simultaneously e-tax payment |

||||||||||||||||||||||||||||||||||||||

|

e-tax payment on subsequent date |

||||||||||||||||||||||||||||||||||||||||

|

Details of payment of tax deducted at source (amount in Rs.) |

||||||||||||||||||||||||||||||||||||||||

|

TDS (Income Tax)(Credit of tax to the deductee shall be given for this amount) |

||||||||||||||||||||||||||||||||||||||||

|

Interest |

||||||||||||||||||||||||||||||||||||||||

|

Fee |

||||||||||||||||||||||||||||||||||||||||

|

Total Payment |

||||||||||||||||||||||||||||||||||||||||

|

Total payment in words (in Rs.) |

||||||||||||||||||||||||||||||||||||||||

|

Crores |

Lakhs |

Thousands |

Hundreds |

Tens |

Units |

|||||||||||||||||||||||||||||||||||

|

Unique Acknowledgement no. (generated by TIN) |

||||||||||||||||||||||||||||||||||||||||

*To be updated automatically

**In dd/mm/yyyy format”.

[Notification No. 67/2022/F. No. 370142/23/2022-TPL]

ANKIT JAIN, Under Secy.